ECA INSIGHT >>

Energy network infrastructure plays a major role in supporting energy system decarbonisation, and potential solutions across several energy vectors are increasingly being considered for future investments. The concept of a Whole System Approach has been on European regulators’ radars for several years now, but the need to move from concept to implementation is more pressing than ever.

The publication of the European Commission’s proposed Hydrogen and Gas Market Decarbonisation Package in December 2021 aims to ease some regulatory barriers to hydrogen investments and further reinforces the need for energy system integration. Regulators will soon be called to decide across electricity, gas and hydrogen network investments, so a whole system appraisal of such investments must be developed. Ideally, this would be harmonised across EU Member States.

The need for a whole system approach

For energy systems to move towards decarbonisation, network investments must help introduce or optimise energy sources (and applications such as heat and transport) in terms of both efficiency and carbon intensity. The search for the most cost and carbon effective investments will need to consider solutions across different energy vectors ie gas, electricity, hydrogen and likely also water and waste. This is a whole system approach, and it requires a common way for regulators to cost and compare the investments proposed by gas, electricity, and hydrogen network operators.

An example of a whole system approach

Consider a gas pipe feeding a small town, which is reaching the end of its asset life. A whole system approach (WSA) would entail examining potential solutions in other energy vectors beyond the gas network. The optimal investment might involve:

● Replacing the pipe like-for-like; or

● Converting the town to electric heating; or

● Installing a biomethane plant and upgrading the gas network.

A cost benefit analysis (CBA) of these options cannot be undertaken by a single network or system operator as it involves potential solutions across both the electricity and gas networks.

WSA developments in the EU

Recently it has become clearer that regulators need to coordinate with the gas, electricity and hydrogen transmission system operators (TSOs), and also the distribution system operators (DSOs), to develop a harmonised methodology for the comparison of whole system solutions.

The proposed Gas Decarbonisation Package not only reiterates the requirements for integrated Ten Year Network Development Plans every two years, but also calls for ENTSOE, ENTSOG and ENNOH[1] to cooperate ‘on the development of the energy system wide cost benefit analysis’ (Regulation, Article 43, paragraph 3).

Some examples of early movers in the EU include the Slovene, Italian and Portuguese regulators who have incentivised some pilots of whole system solutions:

• In Italy, the telecom infrastructure of gas smart meters is shared with other public services such as water and waste management.

• DSOs in Portugal are asked to share their network infrastructure with telecom companies. ERSE, the Portuguese regulator, is currently developing the remuneration structure and the extent of benefit sharing with DSO customers.

• In Slovenia, the regulator has been incentivising a WSA in terms of TSO-DSO coordination in smart grid infrastructure. Network operators are granted a percentage of such an investment if it is shown to have a net societal benefit (ie lower network tariffs).

The first steps towards a WSA for EU regulators seem to be focused on the interaction between transmission and distribution networks and have yet to explore the full scope of a WSA for more strategic investments across multiple energy vectors which can support the road to decarbonisation. This has, however, started to take shape in the UK.

A common CBA tool developed in the UK

The Energy Networks Association (ENA) in the UK has developed a Whole System CBA tool and this has been adopted by Ofgem, the UK regulator, for use during the latest price controls (RIIO ED2). This tool and its accompanying methodology are built to accommodate investment appraisal across gas, electricity, hydrogen, transport and heat at both the transmission and distribution level. Any major network investment in the RIIO price controls will need to demonstrate its suitability across other whole system solutions, ie that a proposed investment in the electricity distribution network has been considered alongside, say, a hydrogen investment and has a more favourable net societal benefit. Therefore, the allowances for network utilities are increasingly assessed during the price control and ex-ante where whole system solutions might be relevant.

In addition, these developments have highlighted that net zero plans are also drawn at a more local, bottom-up level, from mayor’s offices and local institutions. The next milestone for the WSA in the UK is for the Local Authorities to be able to access cross-sector knowledge and have a single point of contact through a standardised process, as opposed to reaching out to the gas and electricity TSOs and DSOs separately for solutions to their net zero plans.

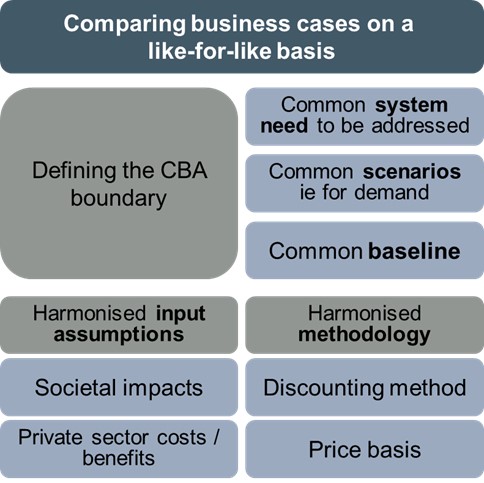

Components of a harmonised WSA appraisal methodology

Regulators need to secure the optimal whole system solutions for consumers. To identify these, they need to be able to compare business cases across different network operators on a like-for-like basis. For example, the CBAs need to value societal impacts using the same assumptions eg carbon prices and sensitivities around these. To compare “apples with apples”, the CBAs should also follow a common methodology for discounting and a common price basis.

It is also important to ensure that the CBAs from different network operators attempt to address the same system need. The coordination of network operators at the outset of the CBA process should mean that the system need is well defined and that they develop solutions to a commonly defined need. Impacts of one network operator’s solution on another network should also be considered, with commonly agreed ways to cost these impacts.

Network operators should also coordinate to identify the reference, or baseline, solution once all potential solutions are identified. Key stakeholders affected other than the network operators and network customers should also be identified with common assumptions regarding their impacts agreed (eg the cost of capital of a generator).

Regulators could choose to develop a harmonised methodology or a common CBA tool, or indeed both, depending on the existing and targeted level of coordination required as energy infrastructure needs arise.

Key challenges

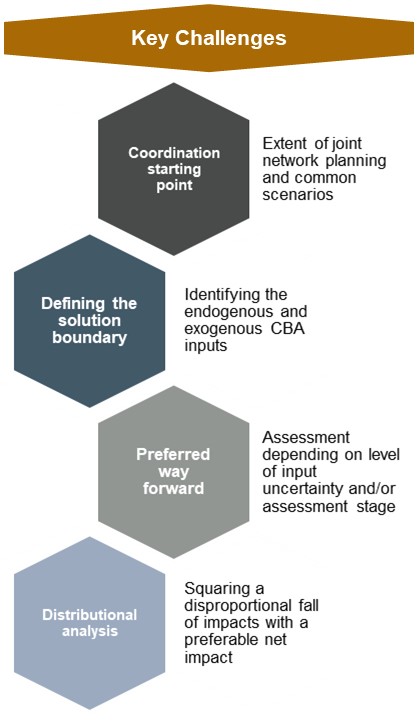

The main challenges to adopting a whole systems CBA include:

● Ensure network operators across energy vectors and transmission and distribution conduct joint or coordinated network planning and develop common scenarios (if they do not do so already). This is a requirement of the recent proposed Gas Decarbonisation Package, which is updated to include hydrogen, however it is still not a reality in many countries.

● Decide whether inputs are endogenous or exogenous, and do so in a consistent manner. For example, the number of electric vehicles might be taken as an exogenous input for a CBA that considers how best to install rapid chargers in an area. However, this might be an endogenous input if the CBA considers how best to decarbonise transport in that area or country, ie the number of electric vehicles should be determined according to each of the solutions to decarbonising transport. Network operators should clearly identify within the CBA which inputs are treated as exogenous and which are endogenous.

● Identify the preferred way forward. The appraisal of the optimal solution may need to consider several assessment methods depending on the context and level of uncertainty around the analysis. These might include the resulting net benefit, a least regrets analysis, or the payback period.

● A distributional analysis would also need to be conducted to illustrate how costs and benefits accrue to different network customers, utilities, other market agents and society. These aspects of the CBA again would need to be harmonised.

Conclusion

The development of a WSA methodology requires the coordination and input of the energy regulators, network operators across distribution and transmission and energy vectors, as well as local communities with plans to meet net zero targets. This could be overseen at the EU level by the Agency for the Cooperation of Energy Regulators (ACER) and / or the Council of European Regulators (CEER) to ensure a harmonised methodology across Member States, as well as a clear governance arrangement.

Steps towards WSAs have so far focused on the interaction between transmission and distribution, whilst the recent Gas Decarbonisation Package seeks to ease barriers towards hydrogen network investments and increase coordination between TSOs and DSOs across all energy vectors in the EU.

The next step to giving effect to a Whole Systems Approach is to develop an appraisal methodology harmonised across energy vectors, where stakeholders determine common analytical methods, tools and assumptions. This will ensure regulators have the necessary tools to decide which network investments best serve consumers in a system with multi-vector options for decarbonisation.

[1] ENTSOE and ENTSOG are the European associations for the cooperation of TSOs for electricity and gas respectively. ENNOH will be created under the recently proposed gas decarbonisation package, as the respective organisation for hydrogen.

Marina Charalambous

Senior Consultant

Marina is an economist with 7 years’ experience in regulatory economics, including energy network regulation, price control and incentives, cost benefit analysis, plus regulatory and commercial due diligence. She has previously worked at the UK energy regulator on the RIIO price controls, then as a consultant advising a range of clients including regulators, utilities, network industry associations and energy infrastructure investors.

To contact Marina directly please email or connect with her on Linkedin below.