ECA INSIGHT >>

The UK capacity market – it gets what it asks for

July 2016

Only a week into the job, Theresa May has already outlined some eye-catching new policy proposals. In the power sector, the industry is on the look-out for hints as to the direction the new Prime Minister and her cabinet will take regarding the ongoing Electricity Market Reform (EMR) process. One clue came in her campaign launch speech where May stressed an energy policy “that emphasises the reliability of supply”. This places the UK’s still developing Capacity Market (CM) firmly under the spotlight.

State of play – more CCGTs please

The latest December 2015 CM auction repeated the first from a year earlier with a low clearing price set by distributed diesel generators. This sparked widespread criticism that such plant will threaten emissions’ targets and hold an unfair advantage from potentially unjustified “embedded benefits”.

The government has made no secret of its desire to see more gas succeed in the next auction and following consultation a number of adjustments have been made to the CM mechanism. But these changes focus on tightening the delivery incentive. We believe a much more fundamental question should be asked – is the CM designed to actually procure what the system needs?

Peak capacity is the wrong parameter

The CM was justified by the need to ensure sufficient flexible capacity is developed in a system with high levels of variable renewable generation. As acknowledged at the time, flexible generation may be required at various intervals throughout the day, rather than only at peak.

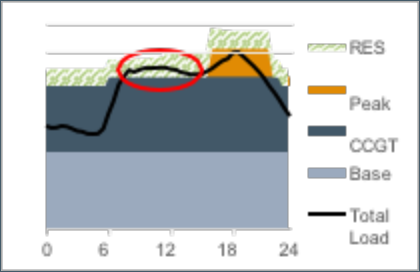

Figure 1 provides a stylised representation of a potential diurnal load profile in October 2020. The system may be in need of flexible capacity at any point renewables are otherwise relied upon to meet demand (eg – the area circled in red). As shown, this could be during the daytime as well as at peak.

Figure 1. October 2020 – possible daytime shortages

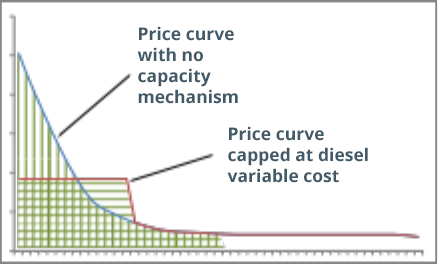

Additional CCGTs may meet this frequent demand for flexible output more economically than peak-focused diesel generators. But as long as the CM auctions for peak capacity, peak focused plants are what it will get. As a result new mid-merit CCGTs are pushed out of the market since diesel variable cost is effectively capping their return in the energy market (Figure 2).

Figure 2. Missing money for CCGT

The firm energy option

A firm energy CM will match the product auctioned with the true desired outcome. Hydro-dominated systems in South America have long adopted this approach to deal with potential dry years. Firm energy looks at deliverability across the year rather than just at peak – it covers peak so can do the same security job as the current CM while giving the right incentives to plant capable of economically supplying power at other times also. Peaking diesel cannot provide sufficient firm energy without excessive SOx and NOx emissions.

A firm energy mechanism may take the form of a distributed load obligation, capacity payments, or a reliability option (as in Colombia). The underlying requirement is that the mechanism is backed by firm generation (based on a probabilistic calculation across the full supply curve) according to its ability to offer firm energy across the year, not just at peak.

Or leave it to the market

The government developed the CM after deciding that the energy market cannot with current interventions be relied upon to deliver sufficient investment in new capacity. However, the current design does not target what is most needed – flexible firm energy rather than simply peak capacity. This flaw lies at the heart of the difficulties new CCGT plants have experienced in the auctions to date. If a CM is to be retained then it should instead value mid-merit operation by focusing on the procurement of firm energy. Else if the increase in centralised procurement and planning this entails is not desired, price signals need to be restored to the energy market by removing the CM altogether.